Chart image provided by the editor; underlying source shown in image as China's National Bureau of Statistics, via Bloomberg.

China's housing crisis is not over. It has changed shape. The most dramatic developer defaults and unfinished-project headlines may no longer be new, but the deeper problem remains: prices are still soft, buyers remain cautious, developers are still constrained, local governments are under fiscal pressure, and the population picture makes a return to the old housing boom unlikely.

As of June 22, 2026, my view is that China's housing crisis is still getting worse in slow motion. It is not necessarily worsening as a sudden financial panic. It is worsening as a long economic drag: lower property investment, weaker household confidence, pressure on city finances, falling land revenue, and a housing stock that no longer matches the country's demographic future.

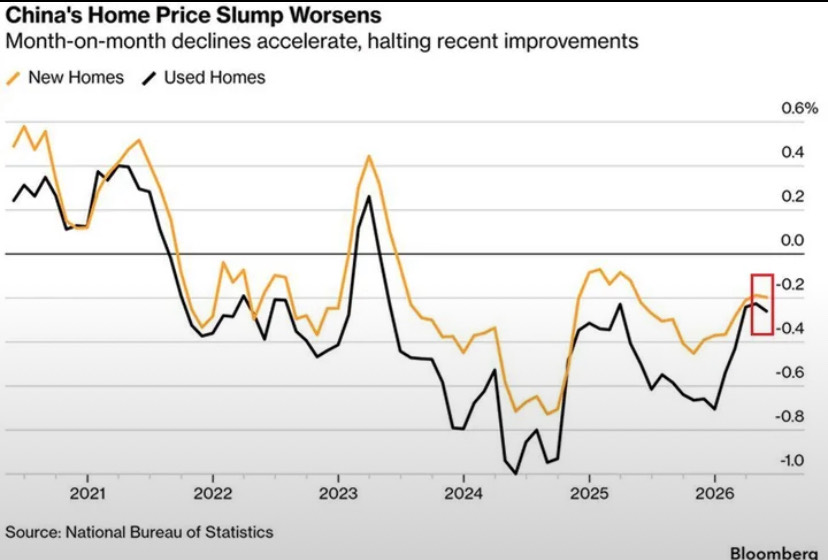

The latest signal: home prices are slipping again

The chart above captures the important near-term story. After brief signs of improvement, month-to-month price declines have reappeared. China's National Bureau of Statistics reported its May 2026 70-city home price data on June 16. The data show that weakness remains broad, especially outside the strongest first-tier markets.

Trading Economics, which tracks the NBS housing index, summarized the latest reading this way: new home prices across 70 cities were down 3.5 percent year over year in May 2026, marking the 35th straight month of decline. On a month-to-month basis, the index fell 0.2 percent after a 0.1 percent decline in April. That is not a crash, but it is also not stabilization.

The first-tier cities are not all behaving like the rest of the country. Shanghai has been firmer than many weaker cities, and recent NBS data showed modest monthly gains in some first-tier markets. But that is exactly the point: China does not have one housing market. It has a few markets with real scarcity and deep employment bases, and many lower-tier cities with excess supply, weaker job prospects, aging populations, and heavy local debt.

Sales and investment are still weak

Prices matter, but sales and investment tell us whether the machine is restarting. On that front, the data remain poor. In its June 17 release on real estate development from January to May 2026, the NBS reported that the floor space of newly built commercial buildings sold fell 10.8 percent year over year. Residential floor space sold fell 12.1 percent. Sales value of newly built commercial buildings fell 13.5 percent, while residential sales value fell 14.1 percent.

That matters because China's old property model required steady turnover. Developers borrowed, bought land, sold apartments before completion, used cash from new projects to finish old ones, and fed local-government land revenue along the way. When sales slow for years, the whole chain tightens.

The same NBS release showed continued stress in development activity. Property investment and new construction have not recovered in a way that would suggest a normal cycle bottom. Fewer starts today mean less steel, cement, appliances, construction employment, land purchases, and local revenue tomorrow.

The national economy is holding up better than housing

China's national economy is not simply the housing market. That distinction is important. Exports, manufacturing, electric vehicles, batteries, solar, industrial automation, and high-tech supply chains can still support headline growth even while property remains weak.

That is why China's economy can look better than its housing market. A weak housing sector does not automatically mean a national collapse. But housing still touches household wealth, local-government finance, construction employment, bank balance sheets, consumer confidence, and demand for goods such as furniture, appliances, flooring, fixtures, and building materials.

The OECD's 2026 outlook for China expects growth to slow and explicitly notes that real estate investment will continue to contract and prices will fall. That is a sober baseline: not a 2008-style global banking panic, but a persistent drag on domestic demand.

Local governments are part of the housing problem

Local-government debt is one of the most important pieces of the crisis. For years, many cities relied heavily on land sales and land-backed financing. Developers bought land, local governments received revenue, and local government financing vehicles, or LGFVs, borrowed to build infrastructure and support growth targets.

When developers stop buying land at boom-era prices, that model breaks. Cities still have obligations: infrastructure, payroll, services, debt service, transport systems, industrial parks, and local development projects. But the land-sale engine that helped fund them is weaker.

The IMF's 2025 Article IV consultation on China, released in 2026, described spillovers from the property sector to local-government finances and debt as a source of continued weakness in domestic demand. The IMF also said unsustainable LGFV debt needs restructuring through insolvency frameworks, while warning that financial-sector spillovers must be handled carefully. The IMF release is worth bookmarking: IMF China Article IV consultation.

A useful way to think about it is this: the housing crisis is not only a developer crisis. It is also a city-finance crisis. Some cities built around the assumption that population, land values, construction, and credit would keep expanding. That assumption no longer works everywhere.

Population decline makes a fast rebound harder

Demographics are the slowest but probably most decisive part of the story. The NBS 2025 Statistical Communique reported that China's population fell by 3.39 million in 2025 to 1.40489 billion. Births were 7.92 million, while deaths were 11.31 million. Urban permanent residents still numbered 953.80 million, but the national population is shrinking and aging.

Housing demand is not only about the number of people. It is about household formation, migration, jobs, income expectations, marriage rates, urbanization, and confidence. But a shrinking population changes the background math. It becomes much harder to justify endless construction in lower-tier cities if the young working-age population is not growing.

Rhodium Group's recent demographic analysis estimates that China could lose nearly 60 million people over the next decade. Even if that estimate is off, the direction is clear: demographics no longer support the idea that every city can build its way to prosperity.

The crisis is uneven by city tier

China's largest cities still have advantages: jobs, universities, hospitals, finance, technology, infrastructure, and migration from smaller cities. Beijing, Shanghai, Shenzhen, and Guangzhou can stabilize sooner because they still attract talent and capital, even if affordability is stretched.

Lower-tier cities face a harder problem. Many have already built too much. Some have weaker job markets. Some depend more heavily on land finance. Some face outmigration of young people. Some have large stocks of vacant or unsold homes. In those places, a modest national easing policy may not be enough to create real demand.

This is why national averages can mislead. A small rebound in Shanghai does not solve the balance-sheet problem in a smaller inland city with too many apartments, aging residents, weak local finances, and a developer that has stopped finishing projects.

Policy support has not been decisive enough

Beijing has tried many forms of support: lower mortgage rates, relaxed purchase restrictions, local rescue measures, encouragement for state-backed buyers, and efforts to convert some unsold housing into affordable housing. These policies can slow the decline, but they have not yet restored the old confidence loop.

The core issue is trust. Buyers need to believe the apartment will be finished, the developer will survive, the price will not keep falling, and their household income is secure. Developers need access to financing and a reason to start new projects. Local governments need revenue. Banks need confidence that collateral values are not still deteriorating.

Policy can help, but it cannot easily recreate the belief that housing is a one-way bet. That belief was the foundation of the old model.

Where to track whether it is getting better or worse

Anyone trying to follow China's housing crisis should watch a small dashboard rather than one headline.

Home prices: Start with the NBS monthly latest releases, especially "Sales Prices of Commercial Residential Buildings in 70 Medium and Large-sized Cities." Trading Economics also has a readable China housing index page.

Sales and investment: Track the NBS monthly real estate development release. The important fields are floor space sold, sales value, residential sales, property investment, construction starts, completions, and developer funding.

Local-government debt: Follow the IMF's China Article IV reports, especially discussion of LGFVs and local-government finance. The IMF country page and Article IV releases are better than most headline summaries.

Developer stress: Watch major private developers, offshore bond restructurings, state-backed developers such as Vanke, court proceedings, and whether unfinished projects are being delivered.

Population and household formation: Use the NBS statistical communiques, the annual population sample surveys, and demographic research from groups such as Rhodium Group, RAND, and the United Nations.

Broader economy: Watch retail sales, fixed-asset investment, unemployment, exports, CPI/PPI, household deposits, mortgage lending, and consumer confidence. Housing cannot be separated from household expectations.

My view: worse, but not in the simple crash sense

The best answer is that China's housing crisis is still getting worse structurally, even if it is not worsening every month in every city. The old property growth model has broken. Prices are still declining in many markets. Sales and investment remain weak. Local governments have less land revenue and more debt pressure. Demographics are moving against broad-based housing demand.

At the same time, China has tools that many crisis countries do not: capital controls, state banks, administrative control over credit, state-owned enterprises, local directives, and the ability to stretch losses over time. That means the crisis may not look like a sudden Western-style housing bust. It may look like years of lower growth, weak confidence, partial bailouts, hidden losses, city-by-city divergence, and slow balance-sheet repair.

The bullish case is that first-tier cities stabilize, policymakers absorb excess inventory, local debt is restructured gradually, and the economy shifts toward manufacturing, services, technology, and consumption. The bearish case is that lower-tier oversupply, shrinking demographics, local fiscal stress, and weak confidence keep dragging on growth for much longer than officials expect.

Right now, the bearish case still has more evidence. The crisis is not just about apartments. It is about a growth model that used property, land, debt, and expectations as a flywheel. That flywheel is no longer spinning the same way.

This article is general economic commentary and not investment advice.