The May jobs report, released today on June 5, 2026, was stronger than expected. That matters because it changes the tone of the interest-rate conversation. A weak jobs report would have given the Federal Reserve more room to talk about cuts. This report does almost the opposite.

The Bureau of Labor Statistics reported that nonfarm payroll employment increased by 172,000 in May, while the unemployment rate held at 4.3%. That was well above the roughly 80,000 to 85,000 jobs many forecasters expected. Revisions also made the prior two months look better, adding 93,000 more jobs to the March and April totals.

The headline number was strong, but the report was not perfect. Financial activities lost jobs, and wage gains remain part of the inflation discussion.

Why this makes rate cuts harder

The Federal Reserve has two big jobs: keep inflation under control and support maximum employment. When the job market looks weak, the Fed can become more willing to cut interest rates. When hiring is solid and unemployment is steady, the Fed has less reason to rush.

This report makes the employment side of the mandate look reasonably healthy. That shifts attention back toward inflation. If inflation is still running above the Fed's comfort zone, a strong labor market gives policymakers more patience. They can wait longer before cutting, and they can even talk more seriously about whether policy is tight enough.

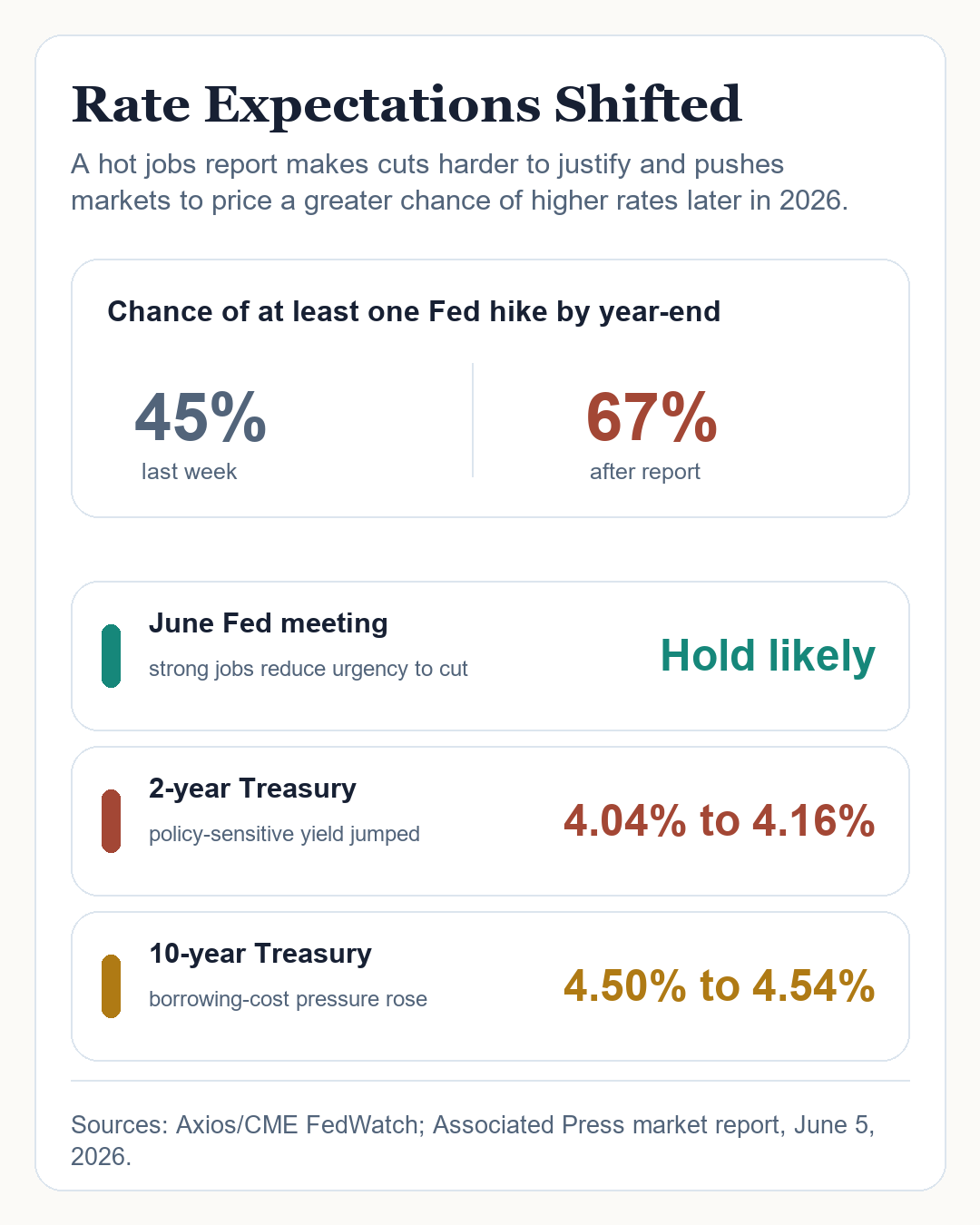

That is why markets reacted so quickly. According to reporting that cited CME FedWatch, the odds of at least one Fed rate increase by year-end rose to 67% after the report, up from 45% the prior week. The Associated Press also reported that the two-year Treasury yield, which is especially sensitive to Fed expectations, jumped from 4.04% just before the report to 4.16%. The 10-year yield rose from 4.50% to 4.54%.

The immediate market message was simple: fewer hopes for cuts, more concern that rates may need to stay high or move higher.

What it means for households

For workers, the report is mostly good news. More hiring means more income, more confidence, and less fear that the economy is about to roll over. A 4.3% unemployment rate is not a crisis level.

For borrowers, it is less comfortable. Higher rate expectations can keep mortgage rates, auto loans, business loans, and credit-card rates under pressure. Even people who are not borrowing directly can feel it through housing affordability, business investment decisions, and stock-market volatility.

The tricky part is that the same data point can be good for jobs and bad for rate relief. A strong labor market helps households earn income, but it also gives the Fed less reason to make money cheaper.

What it means for stocks

Stocks do not always dislike strong jobs reports. In normal times, more people working can mean more spending and better corporate revenue. But when inflation is the main worry, strong employment can become a problem for investors because it raises the chance of tighter monetary policy.

That is especially important for expensive growth and technology stocks. Higher yields make future profits less valuable in today's dollars, and they give investors more competition from bonds. That helps explain why a good labor-market report can still produce a negative day for parts of the stock market.

The bigger picture

The report does not prove the economy is booming. There are still soft spots. Financial activities lost 22,000 jobs in May. Inflation and energy costs remain a concern. Some white-collar hiring has been uneven. And if rates stay high for longer, that can eventually slow housing, credit, and business investment.

But the report does make one thing clearer: the economy is not giving the Fed an obvious excuse to cut rates right now. The June Fed meeting is still widely expected to be a hold. The bigger change is the path after June. The debate is moving away from "When do cuts start?" and closer to "Can the Fed stay patient, or will inflation force another hike?"

That is not the rate relief borrowers wanted. But it is also not the recession signal people feared. It is a strong-enough jobs report to keep the economy moving, and a hot-enough report to keep interest rates uncomfortable.

Sources and notes

Sources used for this article include the BLS May 2026 Employment Situation, Kiplinger coverage of the May jobs report, Axios reporting on rate expectations and CME FedWatch, and the Associated Press market report from June 5, 2026.