This is a 2026 update to the 2013 article Reasons the Economy will not go into Recession Soon. The original argument was simple: confidence matters, jobs were improving, housing was helping, and the economy had more forward motion than the recession warnings suggested.

The same kind of question is worth asking again in 2026, but with more caution. The economy does not need to be perfect to avoid recession. It needs enough income, hiring, production, credit, and confidence to keep weakness from feeding on itself. On that narrower question, the current data still gives several reasons to think a recession is not the most likely immediate outcome.

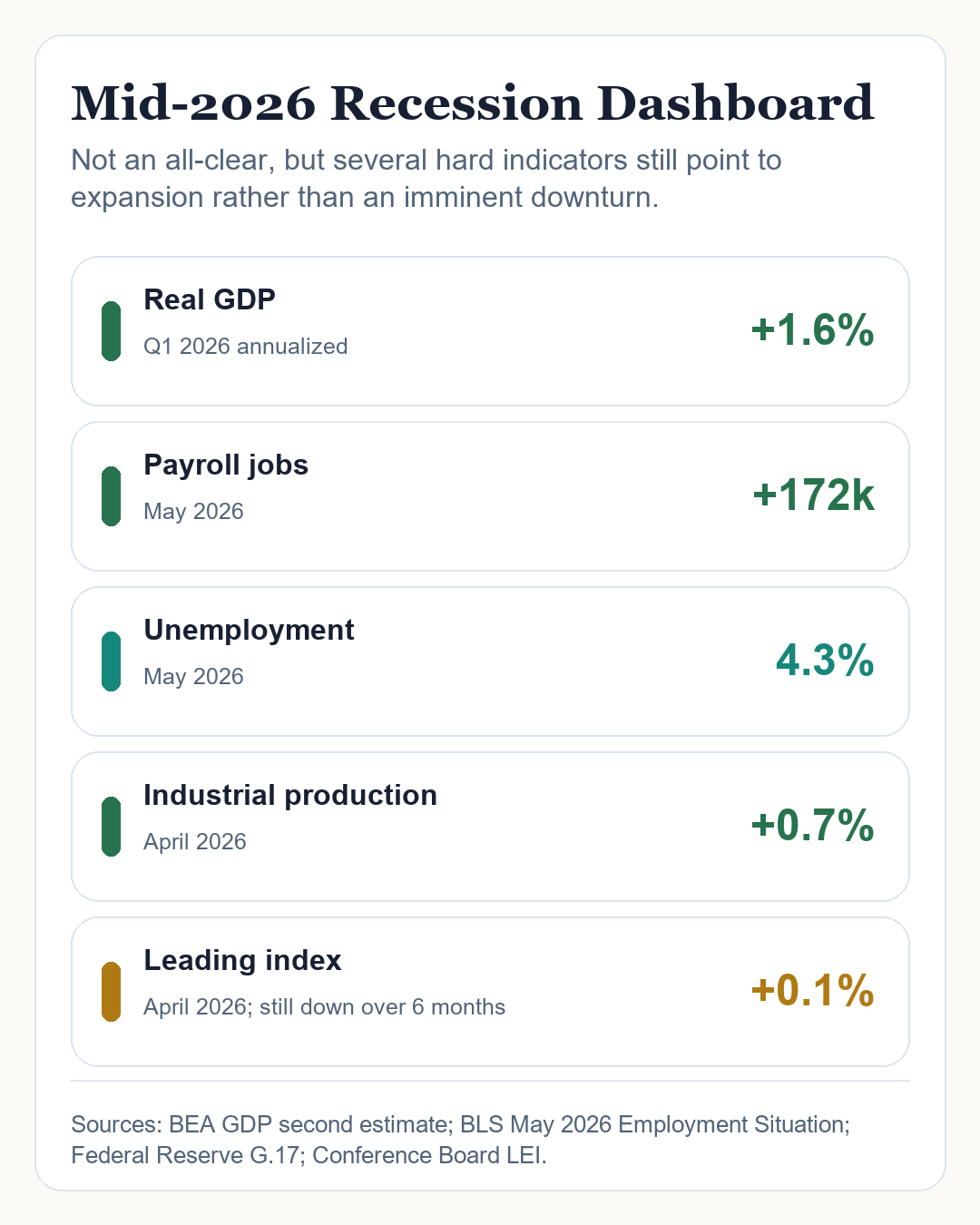

The labor market is cooler, but not broken

In April 2013, when the original article was written, the Bureau of Labor Statistics reported that payroll employment had risen by 165,000 and unemployment was 7.5%. That was an economy still healing from the financial crisis.

In May 2026, BLS reported a very similar payroll gain of 172,000 jobs, but with unemployment at 4.3%. That does not mean everything is easy for households. It does mean the labor market is not yet acting like the beginning of a classic recession, where layoffs accelerate and unemployment climbs quickly.

The 2026 labor market is not booming everywhere, but the unemployment rate remains far below the level in the original 2013 snapshot.

Growth is slower than ideal, but still positive

The Bureau of Economic Analysis estimated that real GDP increased at a 1.6% annual rate in the first quarter of 2026. That is not the kind of growth that makes people euphoric. But recession is usually about contraction, not merely slower expansion.

The Federal Reserve's industrial production report also showed a positive signal: industrial production increased 0.7% in April after a March decline. Manufacturing and production data can be noisy, but this is still a useful check against the idea that the real economy is already rolling over.

The leading indicators are the warning sign

The main reason not to get too comfortable is the Conference Board Leading Economic Index. It rose slightly in April 2026, but it was still down over the prior six months. That makes the picture mixed. The hard data says the economy is still expanding; the leading data says momentum is not strong enough to ignore downside risk.

Several hard indicators remain expansionary, while the leading index keeps the recession-risk argument alive.

Why recession may still be avoided

First, people are still working. A recession becomes much harder to avoid when households lose wage income and businesses respond by cutting more workers. So far, the employment data does not show that kind of self-reinforcing break.

Second, the economy is still producing more. Slow real GDP growth can frustrate everyone, but positive growth gives companies and policymakers more room than an outright contraction would.

Third, some of the old 2013 logic still applies. Confidence can become self-fulfilling in both directions. If businesses keep hiring and households keep spending carefully, the economy can muddle through even when people are worried.

Fourth, the scary story and the optimistic story can both contain truth. Consumers may feel squeezed, interest costs may still hurt, and leading indicators may be soft. But that is different from saying a downturn is imminent. The data in mid-2026 looks more like a slow expansion with risks than a recession already taking hold.

The bottom line

The original article was too casual in saying the economy probably would not go into recession soon, but its instinct was not unreasonable. In 2026, I would phrase it more carefully: the recession risk is real, but the strongest current evidence still points to continued expansion.

The best case is not a boom. It is a boring outcome: hiring continues, inflation pressure does not reaccelerate, production holds up, and confidence improves enough that people stop preparing for a recession that never quite arrives.

Sources and notes

Sources used for this update include the BLS April 2013 Employment Situation archive, the BLS May 2026 Employment Situation, BEA first-quarter 2026 GDP, the Federal Reserve G.17 industrial production release, and the Conference Board Leading Economic Index.